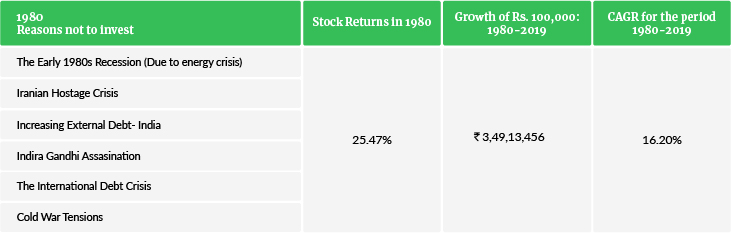

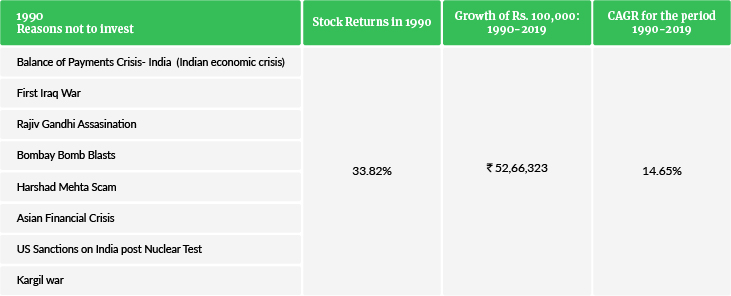

There will always be reasons for not investing or being out of the market

Amar Pandit , CFA , CFP ![]()

October 13, 2020 | 7 Minute Read

Amar Pandit , CFA , CFP ![]()

October 13, 2020 | 7 Minute Read

Amar Pandit , CFA , CFP

![]()

Before you imagine the future, let us go back to 1995.The defining moment for many was the birth of the internet.How many of us would have been able to bet on the Internet?How many.... Read More

6 July, 2021 | 6 Minute Read

Amar Pandit , CFA , CFP

![]()

Can you take a guess about the industry I am referring to? The award clearly goes to the Banking industry. It is an outstanding business and here is my oversimplified take on it. T.... Read More

13 April, 2021 | 5 Minute Read

Amar Pandit , CFA , CFP

![]()

It has been slightly over a year now since COVID-19 created havoc in the lives of people and the way we live, work and play. I distinctly remember March 2020 but do not feel it any.... Read More

16 March, 2021 | 7 Minute Read

To install this website on the Home Screen tap on  and then tap on Add To Home Screen!

and then tap on Add To Home Screen!

Our posts are designed to keep you informed and keep your investment anxieties at bay. Subscribe Now!

0 Comments