What Wise Investors Actually Do In Scary Markets

Amar Pandit , CFA , CFP ![]()

March 3, 2026 | 7 Minute Read

On February 28, 2026, the world woke up to one of the most consequential geopolitical events in years. In a highly provocative move, the United States and Israel launched coordinated airstrikes deep inside Iran. These strikes hit strategic military and leadership targets in Tehran. According to multiple reports, the Iranian Supreme Leader Ayatollah Ali Khamenei was killed along with several senior commanders.

Within minutes, global markets reacted. Oil prices jumped sharply. Safe-haven assets rallied. Equities slid. Currencies shifted. Headlines blared from Mumbai to Manhattan about “war risk premium,” “energy disruptions,” and “geopolitical shock.”

In moments like these, investors are confronted with uncertainty, fear, and noise and how people behave emotionally and financially often determines their long-term outcomes more than the event itself.

Let me share a story.

Gaurav is a mid-40s corporate professional who has been investing for 15 years. He is diligent, hardworking, and disciplined. But like most of us, his emotional wiring around money is far from perfect.

He had built a diversified portfolio of equities, fixed income, gold, and a small allocation to commodities. For years he diligently contributed every month, reviewing his asset allocation once a year, and never overreacted to market noise until now.

When the news broke of the strikes on Iran and the reported death of its supreme leader, Gaurav’s phone lit up:

Sensex down 1000 points in early trade.

Brent crude up nearly 10%.

Gold up sharply.

Safe-haven currencies strengthening.

His WhatsApp groups were full of panic.

One friend said: “Sell everything now. This could be World War III.”

Another said: “Run to gold and stay in cash till peace returns.”

Gaurav felt a familiar knot in his stomach.

On Monday morning, before markets opened, he called his financial coach.

“I can’t sleep. My portfolio is down. What if this escalates? Should I sell to lock in losses and come back later?”

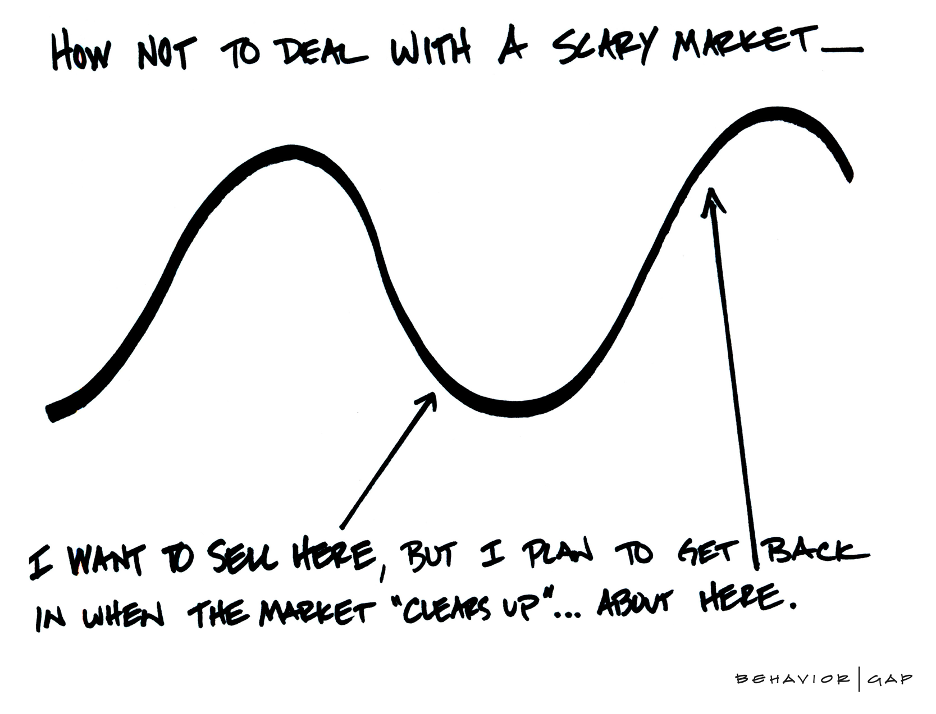

That sentence captures the emotional trap most investors fall into: wanting to avoid fear so badly that they also avoid opportunity.

When geopolitical risk surges, markets do what markets always do; they price uncertainty.

Oil prices rose sharply, driven by fear that conflict could disrupt flows through the Strait of Hormuz, a critical chokepoint for global energy trade, where nearly 20% of global crude and LNG flows.

Equities especially risk assets sell off because investors require a higher risk premium for holding uncertain exposures. Safe-haven assets like gold and Treasuries benefit because they are perceived to store value when fear spikes.

But here’s the nuance that many miss:

Market reactions are almost always immediate, emotional, and exaggerated but long-term fundamental shifts require sustained developments.

Temporary spikes in geopolitical tensions do not automatically translate into permanent changes in economic fundamentals. What matters for long-term investors is whether events change real economic growth, corporate earnings, or consumer behavior over years. What matters less is a headline shock.

Yet human psychology does the opposite of rational markets.

When fear goes up, rational thought tends to go down.

Gaurav’s reaction is not unusual:

He felt fear first.

He wanted to act quickly.

He wanted certainty.

He wanted control.

Emotionally, this makes sense. Fear triggers a biological stress response. Our ancestors survived by avoiding danger, and that instinct is still wired in us.

But financial markets are not a predator in the grass.

They are a pricing mechanism where fear and greed constantly interplay.

Reacting impulsively to fear often means you crystallize losses.

More importantly, you miss the inevitable rebound phases that follow panic.

When markets price geopolitical risk, they overshoot.

This was true in past conflicts and shocks from the Gulf War to the Ukraine invasion, to the shocks during the global financial crisis.

Markets don’t price proportionally. They price emotionally.

Oil may spike, economies wobble briefly, and stock indices may dip. But human economic activity, supply chains, consumption, and long-term growth drivers rarely disappear because of one event even if gravity and short-term volatility make it feel like everything is unraveling.

Gaurav didn’t know this consciously, so his heart and brain were in conflict.

He was tempted to sell.

But he paused.

He asked a different question:

“What is my time horizon?”

His goal was long-term savings for retirement, education funding, and legacy building all at least 15 to 20 years away. Nothing in this geopolitical episode changed those goals.

That one realization clarity of purpose shifted his perspective.

When a major geopolitical event shocks markets, there are usually four broad possible outcomes:

- Contained escalation with limited fundamental impact: markets rebound once clarity emerges.

- Prolonged conflict with energy supply disruptions: short-term inflation pressure and sectoral rotation.

- Widening regional disruption: heightened risk aversion and safe-haven flows.

- Political resolution or negotiation: reduction in risk premium and market recovery.

Right now, it’s too early to know which scenario will unfold. But history suggests that scenarios 1 and 2 are far more likely than scenario 3 or 4 heading into long-term structural changes.

This does not mean conflict isn’t serious; it means investors should contextualize risk rather than catastrophize it.

The Core principle to remember is that markets are forward-looking.

They price future expectations not current realities.

When news hits, prices move swiftly.

But once the initial risk premium is priced, markets tend to stabilize unless the situation deteriorates structurally.

This is why investors who panic sell often end up missing the eventual re-pricing of reality back toward fundamentals.

When Gaurav completed his call with his financial coach, they did not sell.

They reviewed:

His time horizon.

His risk tolerance.

His asset allocation’s match with goals.

Whether any fundamental changes had occurred in his reason for investing.

The answer was no.

Nothing about the crisis changed what his long-term goals were.

They did something more strategic than selling:

They stayed disciplined.

No knee-jerk rebalancing.

No emotion-driven exit.

A reaffirmation of long-term strategy.

That’s behavior that builds lasting investor advantage.

Most investors fear losing money more than they value missing opportunity.

This bias is called loss aversion.

It makes losses feel more painful than gains feel pleasurable.

When headlines trigger fear, many investors act defensively.

Markets are not personal.

They don’t know you.

But your psychology does.

And if your psychology dominates your decisions, your portfolio will often reflect fear, not strategy.

When you have:

- Clarity of purpose,

- Discipline in process,

- Time on your side,

…you navigate uncertainty with confidence, not anxiety.

Gaurav realized that his portfolio was positioned for his long-term goals: diversified, consistent, aligned.

Therefore, he did not panic.

Instead, he reinforced his contributions.

He reminded himself that markets have volatility, but portfolios have resilience.

And crucially, he reaffirmed his long-term horizon.

Geopolitical events can rattle markets.

They can test conviction.

They can amplify emotions.

But they don’t change the fundamental nature of sound investing:

Markets are volatile in the short term.

Markets are resilient in the long term.

Emotional reactions damage outcomes.

Clarity and discipline enhance them.

In times of uncertainty, don’t ask:

Should I run from fear?

Instead ask:

Does this change my goals? Does it change my plan? Does it change my allocation?

If the answer is no, then volatility is just noise.

And long-term investors who stay committed can weather it with courage, clarity, and calm.

and then tap on

and then tap on

0 Comments